The Shareholder Primacy (SP)

economy of is fundamentally different from the Stakeholder Capitalism (SC)

economy of the postwar era.

Today's economy is not capitalism

operating in a different environments but different species

of capitalism

I have previously written about how

business/economic culture evolves between shareholder primacy (SP)

and stakeholder capitalism (SC) archetypes and presented a model characterizing this evolution. The

economies to which these cultural archetypes are adapted are different from

each other. By analogy to biology we can say that the

economy associated with SP versus SC culture are different species of

economy. The SP economy, which I call neoliberalism, is what we have today. The SC

economy is what we had over 1937-81, which I will call Keynesianism.

The two economies have different

inflationary properties

Both neoliberal and Keynesian economies are examples of market capitalism. They

are often seen as the same, but as I will show here, they are distinctly

different basic characteristics. For example, the two economics have different

propensities to inflation. Inflation in Keynesian economics can be

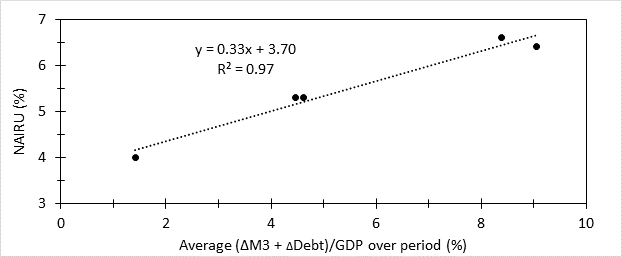

characterized in terms of the Phillips curve, and the NAIRU parameter. NAIRU is

the level of unemployment at which inflation is unchanging. If unemployment

falls below NAIRU the economic is said to be overheating and inflation should

appear after a lag of up to a year or so. If it rises above NAIRU, the economy

is slowing down, heading towards recession, and inflation should begin to fall

withing a few months or less. NAIRU reflects the residence time of money in the economy, that is how long

it hangs around before being spent. A correlation between the two can be used to

estimate NAIRU as a continuous function over time.

In the decades after WW II, a

practice of gradually increasing deficit spending developed and NAIRU rose in

tandem (see Table 1). High NAIRU means higher unemployment levels are needed to

keep inflation under control. Higher unemployment means a lack of worker

bargaining power and reduced prospects for wage growth. It was Democratic

policy under the FDR dispensation that allowed the Keynesian economy

to evolve. Continuation of this dispensation was dependent on the continued

delivery of wage growth to their working class base.

The rise in deficit spending ultimately resulted in the replacement of the FDR

with the Reagan dispensation. With the new dispensation came new economic

policy that selected for SP economic culture, and evolved the neoliberal

economy of today.

Table 1. Average deficit, NAIRU,

unemployment and inflation rates (in %) over time

After 2000, the Phillips curve no

longer holds and NAIRU values can longer be identified. NAIRU values estimated

using the pre-2000 correlation with money residence time are no longer

meaningful. For example, over 2015-19 NAIRU averaged 6.3% due to high levels of

deficit spending while unemployment rate averaged 4.4% suggesting highly

inflationary conditions existed, yet inflation was only 1.9%. An even more

extreme case occurred with the pandemic. Deficits ran at 15% and 12% during the

pandemic years of 2020 and 2021 which was followed by inflation rates of 7 %

and 6% in 2021 and 2022, with a peak of 9% in June 2022. In contrast the

country ran deficits of 12% and 17% over the pandemic years of 1918 and 1919

during which inflation ran at 20% in 1918 and 15% in 1919 with a peak of 24% in

June 1920. Deficits less than a tenth higher during the pandemic a century

earlier produced an inflationary response 2.6 times higher.

Dick Cheney noted in 2002 that “Reagan provided deficits don’t

matter” and with

that statement the Bush administration proceeded to prove the case with their

fiscal policy. Cheney was wrong about Reagan, deficits

still mattered very much in the 1980’s and preventing the inflation they would

otherwise generate required keeping millions of workers unemployed (see Table

1). But he was right than they no longer mattered in the 21st

century, so their plan to cut taxes and run deficits was not going to require

they run the high unemployment policy Reagan did, which might affect their

reelection chances.

Business cycle length is different

also

Table 2 shows that business expansions have grown longer over time, while

recession length has not. During the four decades before the Great Depression

business cycles were short and roughly corresponded to Kitchin cycles which are thought to be driven by inventory

fluctuations. Expansions lengthened during the 1929-1970 Keynesian era.

Business cycle length shortened during the stagflationary

collapse of the Keynesian economy in the 1970’s and then lengthened with the

shift to neoliberal policy after 1980. Average cycle length increased to more

than six years, approaching the length of Juglar cycles.

Juglar cycles are investment driven, characterized by periods of optimism with

a “hot” economy--as indicated by high asset valuations and/or price inflation.

Eventually, rising interest rates or an asset price crash induces a recession

and the business cycle is complete.

Table 2. Economic expansion has

grown longer over time.

The post-2000 economy is fully SP,

with an average business cycle length of about 9 years, fully in the 7-11 year range of Juglar cycles. The figures in Table 2

count the two month NBER recession in 2020 as a normal recession, when it was

anything but. The month before the pull back the stock market had set a new

all-time high, indicating that the economy then was far from recession. The

demobilization of a sixth of the workforce by quarantine rules forced a

reduction in economic activity, which rapidly recovered as soon as businesses

were permitted to reopen. As for the stock market it was up more than 15% in

2020. In many ways we remained in the expansion that began in 2009.

If we assume this, then we are

still in the business cycle that last peaked in 2007, 18 years ago. I have

previously argued that financial crisis is a

normal feature of SP culture, the 2008 crisis was not a fluke and so, will

happen again. Before the New Deal, when financial crises were a normal thing,

they were semi-periodic, with a spacing of 14-22 years (average 18). If we are

indeed in the same business cycle which comes to an end in the next few years

then there would imply today’s business cycle is a Kuznet cycle. These were historical cycles

linked to boom bust cycles in housing investment/construction leading to

periodic financial crisis.

Before the New Deal there were

lesser and greater economic crises Besides the Kuznets panics in 1819, 1837,

1857, 1873, 1893, 1907 and 1929, there were lesser ones that together with the

major panics defined the Juglar cycle. Within the Juglar cycles were the

ordinary Kitchin cycles. Keynesian

economics provided tools through which policymakers could smooth out the

cycles. For example, New Deal policies such as unemployment insurance and SNAP, act as economic stabilizers. This and better inventory

management eliminated the Kitchin mechanism by the 1960’s. Other Keynesian

policy such as illegal stock buybacks and high marginal tax rates served to

prevent asset bubbles, inactivating the Kuznets mechanism and making financial

crises a thing of the past. This left the Juglar as the primary business cycle.

The primary issue was inflation rising during an expansion, forcing interest

rate hikes until the economy went into recession.

That the business cycles after 1960

were shorter than the old Juglar cycles was largely due to the lack of fiscal

discipline that drove NAIRU upwards and made a low-unemployment/high wage

economy impossible to run for another length of time before rising inflation

forced policymakers to induce a recession. This changed with the onset of

neoliberal policy around 1980. Neoliberalism features a “wealth pump” that redirects income that used

to go to workers into building higher asset valuations, what I call “ziggurats of finance.” The positive institutional flows

of money into the ziggurat act as financial stabilizers, reducing the strength

of the driver of non-inflationary Juglar cycles. As mentioned above, the

inflation-resistant nature of the neoliberal business cycle eliminates this

Juglar cycle driver. Thus, the only still active cycle mechanism is recession

following a stock market crash, such as in 2000, also

Neoliberalism eliminates the

mechanism that prevents financial crises. It was only in the mid-1990’s when

the economy became majority SP that the Kuznets mechanism was

reactivated and we got the first of the modern panics in 2008. There are two

interpretations one can draw from this. One is we have reconstituted the

pre-1929 cycle structure, just without the Kitchin cycle component. Here were

would have big recessions every other decade, reflecting the Kuznets real

estate cycle with smaller ones mid-way between

reflecting Juglar cycles. Since 2008 there has been only one Kuznets downturn.

with another expected before the end of the decade, and two Juglar downturns in

2001 and 2020. But if we rule out 2020 as artificial, then what we may have is

a new economy of extremely long expansions that only end with a financial

crisis and severe recession. That is, the wealth pump has eliminated the Juglar

boom and bust cycles altogether, producing a lengthening of the business cycle to

Kuznets length.

Economic performance with respect

to workers is different as well

Table 2 shows that while business

expansions got longer, recessions did not, meaning the economy is in expansion

mode for the vast majority of the time. Average real wage growth over the

period covering in Table 2 was 2.0%. Also shown in the table is the fraction of

the time real wage growth ran at this 2% rate or higher. The longer periods of

expansion have not necessarily resulted in more opportunity for wage increases.

Though the pre-1929 economy was in expansion mode only 55% the time, 70% of

that time wages were growing. Since 2000 the economy has been in expansion over

90% of the time, but wages were growing less than a fifth of the time. The

situation was not all that much better in the three decades before 2000, when

wages grew a little more than a quarter of the time the economy was in

expansion. Compare this to the 73% of expansions showing above average wage

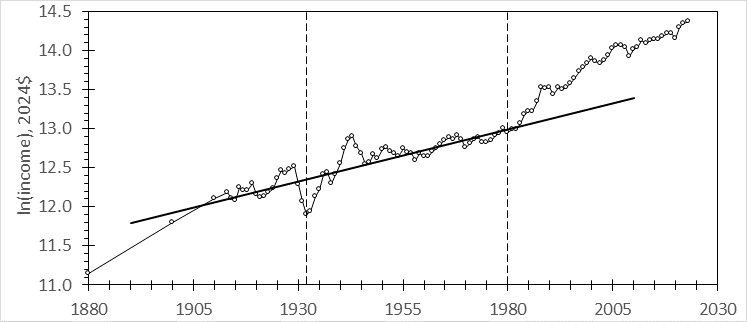

growth for the ninety years before 1970. There is a reason why long-term real

unskilled wage plots (see Figure 1) show a rising trend for almost two

centuries and then flat afterward. Economic policy changed, first in response

to seemingly out-of-control inflation and then in response to a new political order calling for the subordination of

Labor to Capital.

Figure 1. Real unskilled earnings

relative to a value of 64 for the peak year in 2020.

Summary and conclusions

The present neoliberal economy run

in accordance with shareholder primacy culture is fundamentally different in

how it works and what “utility” it seeks to maximize than the Keynesian economy

run under stakeholder capitalism. These differences justify considering them as

different economic species. And they are, in turn, different from the species

of economy that preceded them. Each as evolved from its predecessor as

biological species evolve. But the process involved is cultural not

biological evolution. Biological operates by natural selection, a random,

mindless process that has no direction. Cultural evolution only happens with

people and is not a mindless process, though it often operates in the

background and in ways that are not always understood when they are happening.

The reason why wage growth in

Figure 1 accelerated between 1930 and 1975 was not the result of mindless

external forces but the result of a conscious effort on the part of New Deal

policymakers who were trying to achieve this result, which they achieved by

creating the SC economy. Income shares are zero sum. If more is to go to

workers, less will be left for owners. Compare the income profiles over the

1930-80 period in these figures for the working class and the rich. Outside of the 1930-80 period,

incomes for the rich rose at about the same rate (2.8%) as did incomes for the

working class (3.2%) inside the 1930-80 period. Similarly

outside that period working class wages rose at 1.0%, about the same as the

1.3% rate at which incomes for the rich rose inside the 1930-80. That is,

during the 1930-80 period the rich and the working class traded places and the

rich did not like that one bit.

So when stagflation resulting from

Keynesian policymaker failure destroyed faith in the New Deal political order,

the rich and their Republican allies were able to restore things to “the way things oughta

be” as Rush

Limbaugh put it. And this they achieved by creating the SP economy. The reason

why the economy doesn’t work for ordinary people is because its

not supposed to—it is designed to work for elites. The reason why it

worked for your grandfather or great grandfather is because it was designed to

do so—not because of some deus ex machina reaching out of the sky to

boost the fortunes of the American working class. These good times were the

result of the political order established by the New Dealers,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}